Good morning! The exchange of fire between the US and Iran continued overnight as traffic through the Strait of Hormuz ground almost to a halt. We explore the recent developments in the region in the Strait of Hormuz section. The ongoing energy supply shock is beginning to impact the Fed rate hike decision—the market on the chances of one moved up significantly.

Outside of the Iran war and its consequences, we provide a small update on the midterms, as well as potential new Cabinet members across the pond. Then we move on to tech as we take a first look at Grok 4.5 and its improved capabilities. Lastly, we have a small update for the World Cup fans.

Let’s take a look at the markets to make sense out of the news!

The Midterms Tracker

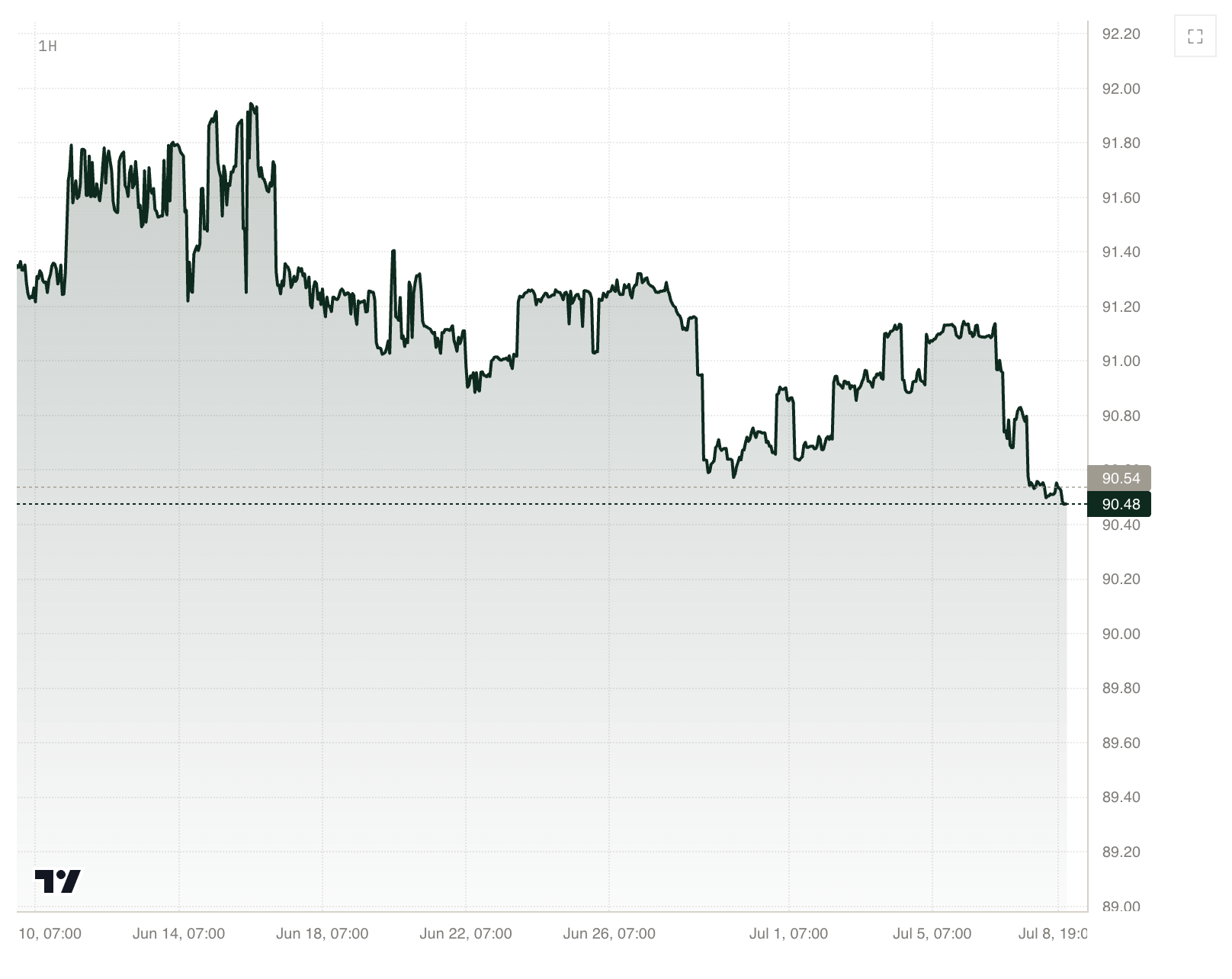

RED

RED is flat on the day and remains around the 90.5-91.5 range.

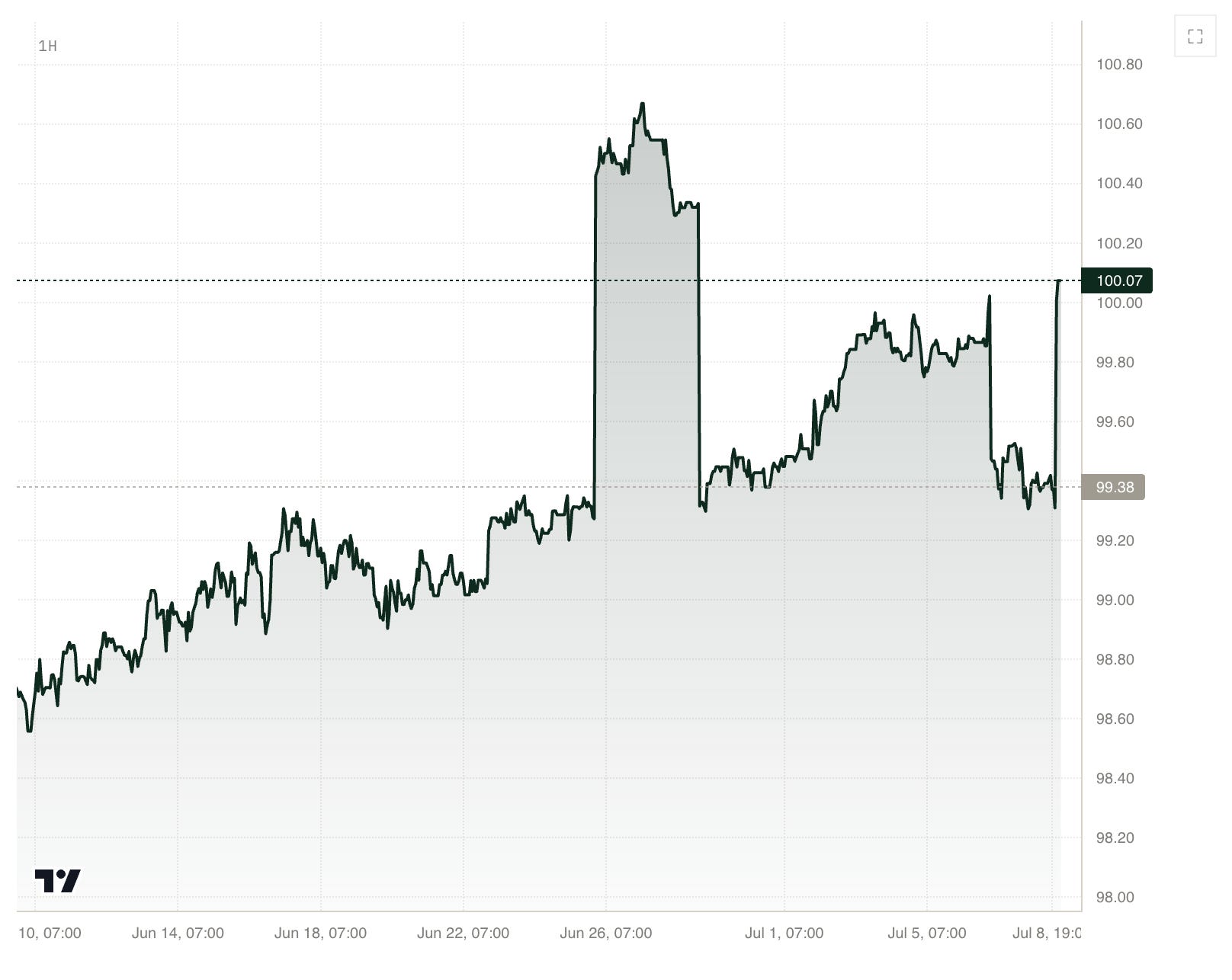

Senate

SENR seems to be back to the slow upward trend after a short slump.

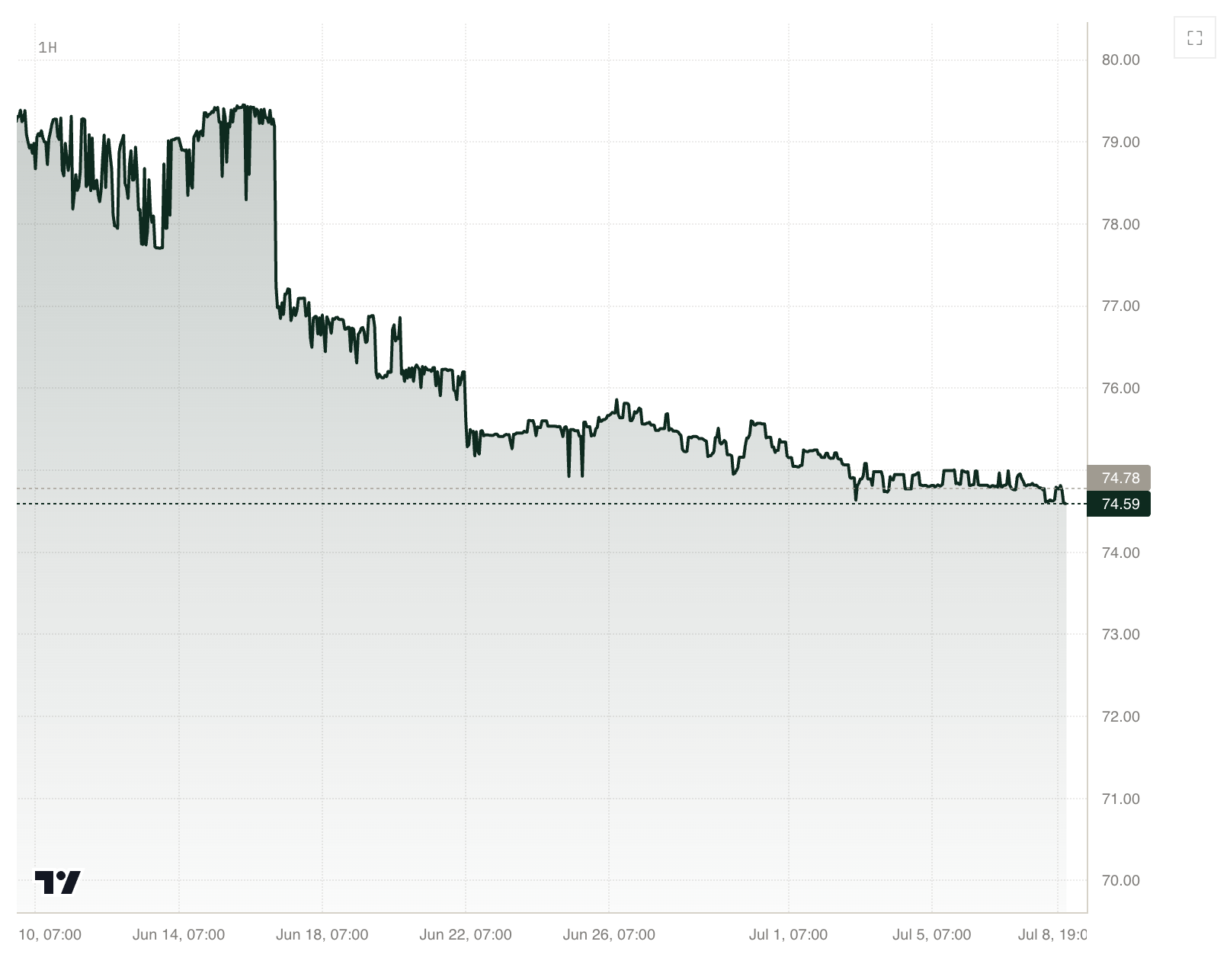

House

HOUSER stabilized around 75 points indicating that Democrats are a strong favorite to win the House in the midterms.

Main Events Of The Day

#1 The Strait Of Hormuz

Yesterday’s strikes continued overnight. Both sides hit multiple targets and neither seems ready to back down. US officials say that even bridges in Iran were targeted this time, along with military sites across the country.

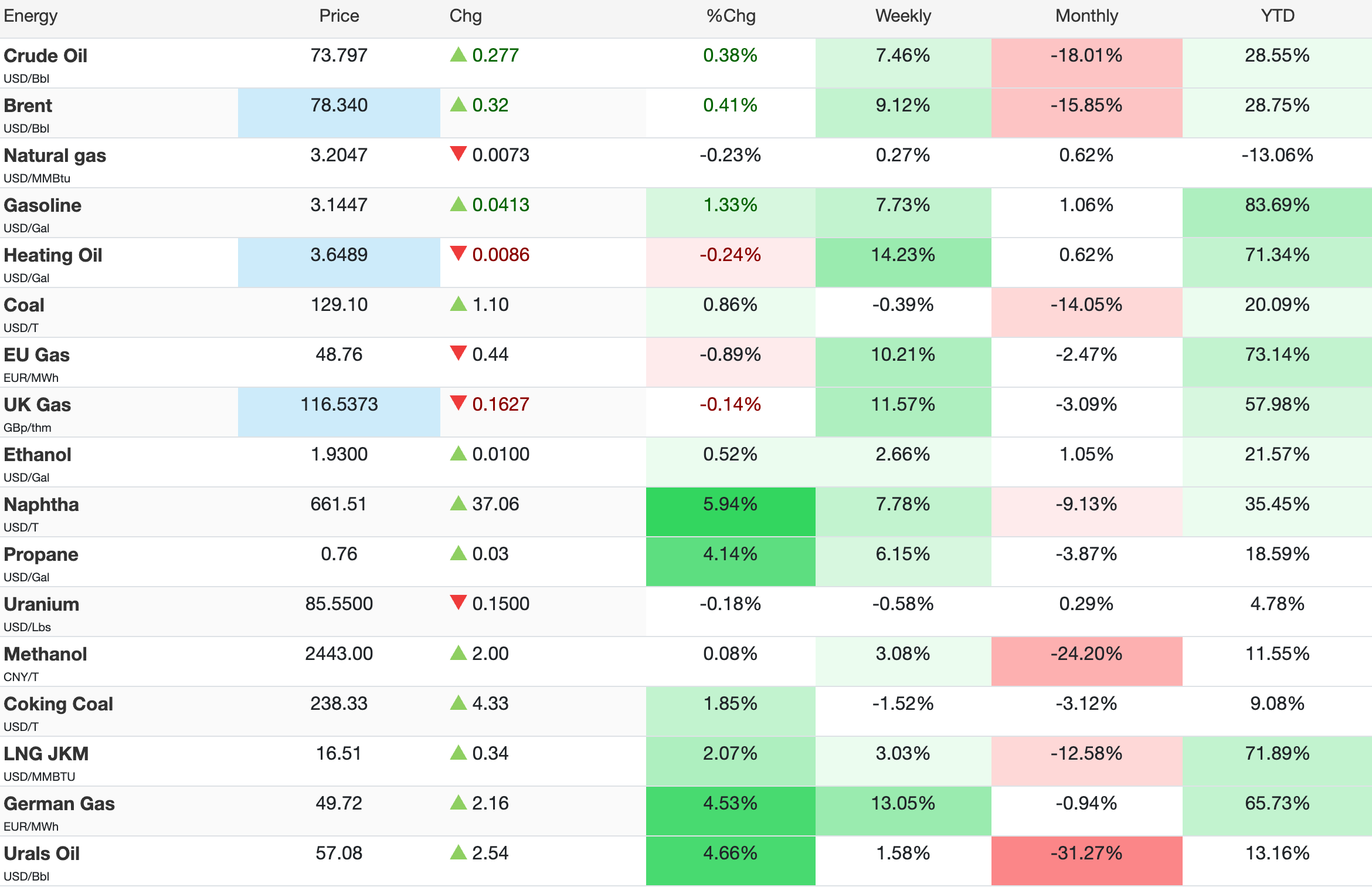

The market on the Strait of Hormuz avoided further decay as traders have already priced in the current level of confrontation. In the meantime, oil is starting to catch up with the reality:

As the hostilities continue, traffic through the Strait becomes more and more difficult:

Without any de-escalation soon, we expect to see further increases in oil prices, combined with the chances of traffic normalization going lower.

#2 Fed Hike May Come Sooner Than Expected

The current situation on the energy market, caused by the Iran war, impacts the Fed. Kevin Warsh started his term in difficult conditions. After months of Trump bashing Powell for not lowering the rates, he must now consider raising them.

The recent FOMC minutes release underscored a deep divide between the board members. However, they also showed a real hawkish turn, compared to previous releases. Traders noticed that and moved their forecast ahead. Now, September meeting is when the decision will be made.

#3 No News Can Be News In Itself

Moving across the pond, we still have no news about the final picks for the Great Offices of State in the UK. Andy Burnham is keeping us in the dark, but some traders perceive it as a signal in itself.

As time goes by, chances of a last minute, dark horse candidate get lower. The public has now digested the rumors and got used to the top names being repeated in the news. It might be the last time we see Ed Miliband priced so low.

#4 New Grok Has Made Some Waves

xAI released Grok 4.5 yesterday in an effort to keep up with the industry leaders. This time, however, the company partnered with the newly acquired Cursor to vastly improve its coding capabilities:

Additionally, the model is rumored to be significantly cheaper than Mythos-class models from Anthropic.

Traders are not expecting a shocking performance in Text Arena though. A score around 1,470 would put the new model just behind the top 10, currently dominated by Anthropic.

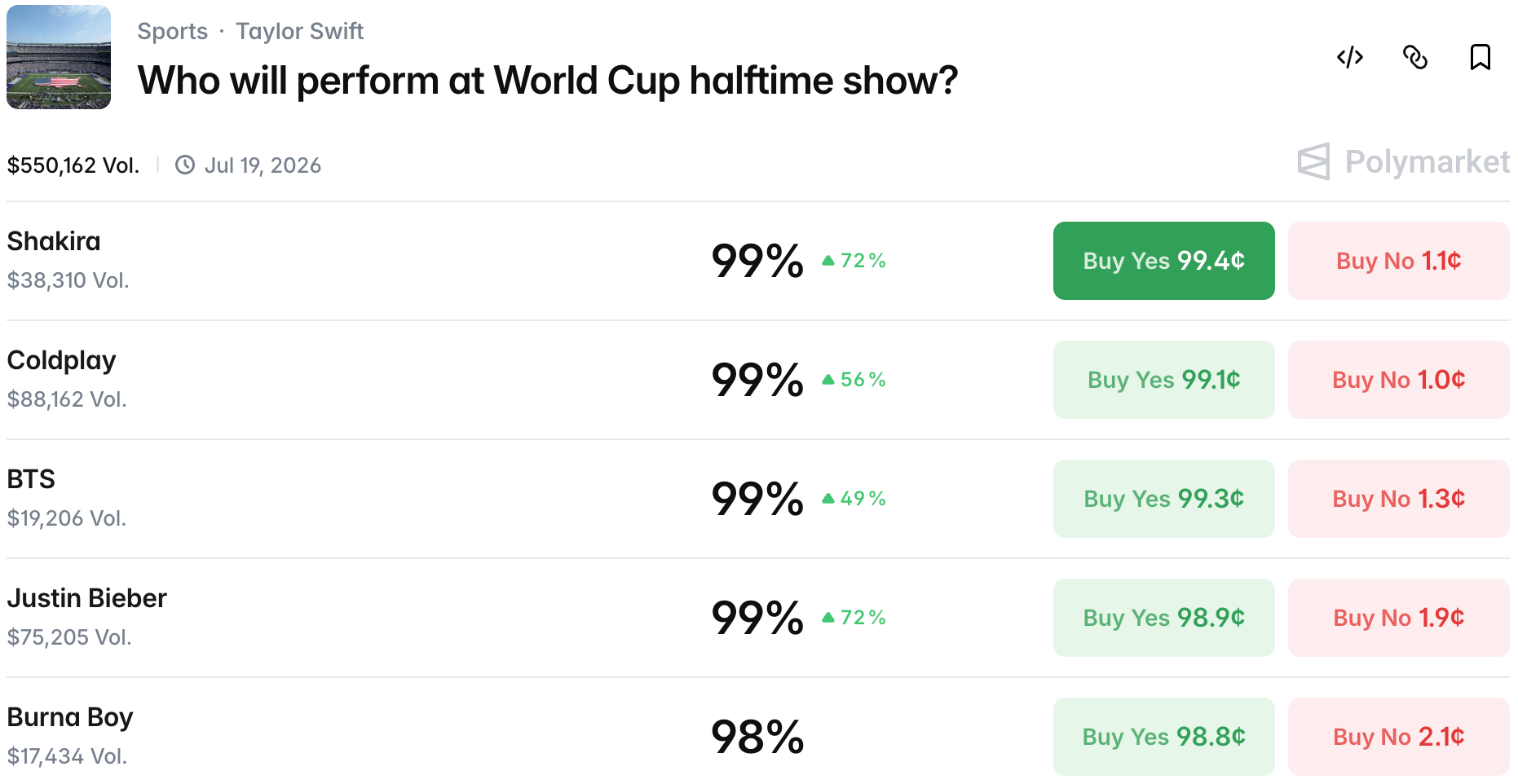

#5 World Cup Final Halftime Show

Lastly, something for soccer fans—Halftime show for the final is now confirmed.

Some names were expected, while others were more surprising, like Shakira, Justin Bieber or Burna Boy. Culture traders had a bit of fun in the market as we are watching the quarterfinals. Do you have your favorites for today’s game?

Wrap up

That’s all for today!

We will continue to monitor the situation on prediction markets.

Make sure to follow prediction markets live to get fresh information on the conflict. Stay strong and see you tomorrow for another Morning Brief!

This is not official investment or life advice. Do your own research. These are only my opinions and I encourage anyone to do their own research before putting any money anywhere.